Sorry for the delayed response Marty. Dealing with Isaac’s steaming pile of --err-- unsubstantiated assertions is proving remarkably time-consuming

Wireless is a meme derided by some as “the magic wireless fairy” (because, from a technical perspective, it’s somewhat fanciful) and a zombie meme (because it’s been buried often, but keeps rising from the grave).

Group peculiarities notwithstanding, overall demand is rising exponentially. In the very near future, no wireless technology will cope with forseeable demands. Wireless has a place, but it’s not a universal panacaea. In some high-value markets, it might be possible to maintain performance by increasing the number of base-stations but we’d eventually end up increasing the field strength to the point that you could use it to cook lunch (slight exaggeration there). Of course, each base-station would need a fibre feed.

To quote from the ABC’s dated, but excellent, coverage:

As more people use smartphones, laptops and tablets to access their emails and the net, the argument that we don’t need to upgrade to fixed-line broadband because “the future is wireless” has sprung up.

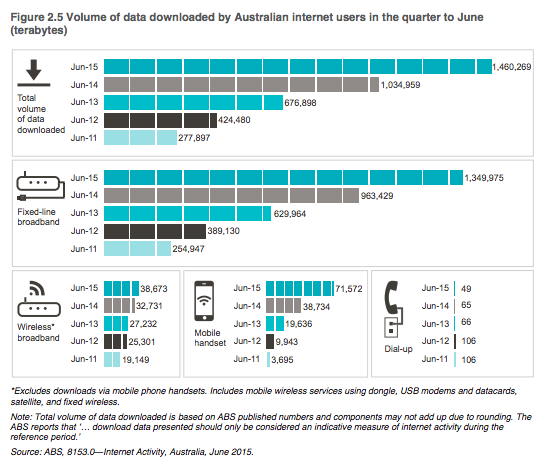

Few experts agree. The consensus is that fixed-line broadband and wireless broadband are complementary technologies and we will need both.

“Wireless use will continue to increase but it is limited by the fact that it uses spectrum and the spectrum is a very scarce resource,” says Mike Quigley, the CEO of NBN Co.

“This is why we’re now seeing a huge shift in countries overseas of getting data traffic off the mobile network and on to the fixed-line network.”

The problem is that the spectrum that supports wireless is limited and the more people who use it, the slower it gets. It’s not a substitute for a good fixed-line broadband network.

People typically find that a couple of children in the family bring home the limitations of wireless. Mobile data is expensive and several users trying to (for example) access video for education or entertainment quickly overloads the available bandwidth. Wireless may be cheap to establish, but it’s very expensive to operate and maintain.

Try not to confuse mobile broadband and WiFi. Both rely on the fixed-line network. If you’re on WiFi, then you’re probably not far from a fixed-line access point. If you’re on mobile broadband and getting reasonable performance, then you’re unlikely to be much further from a base station. Mobile broadband is a function of the mobile 'phone network, which also relies on optical fibre for backhaul.

In infrastructure terms, wireless is an add-on to the fixed-line network. Without fixed-line foundations, you don’ got no wireless.